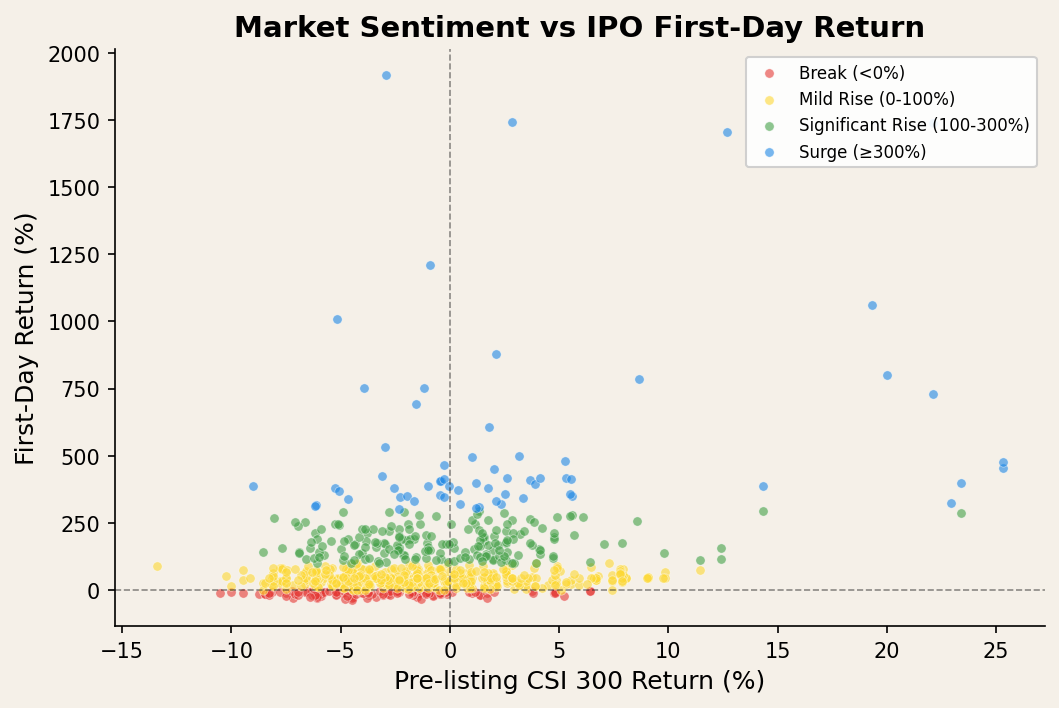

Outcome Specification

Most studies treat IPO first-day returns as a continuous variable (OLS) or binary outcome (underpriced vs. overpriced). In practice, a stock that breaks issue price, one that doubles, and one that triples carry qualitatively different implications for investors.